The post-pandemic recovery initially brought optimism, but as inflation persisted and global conflicts disrupted supply chains, 2025 ushered in a new era of volatility. Public market corrections and rising interest rates reshaped how private equity allocates capital.

Unlike the 2010s — when liquidity was abundant and valuations climbed steadily — today’s environment demands strategic patience. Fund managers are finding that traditional playbooks centered on high leverage and quick exits no longer guarantee strong returns.

According to Preqin’s Global Private Capital Report (2025), nearly 68% of private equity managers now expect longer hold times for portfolio companies, while 55% are reassessing leverage levels to reduce exposure to interest rate risks.

Private equity has transitioned from being an engine of aggressive growth to a discipline of endurance and value creation.

Evolving Time Horizons: From Quick Flips to Long-Term Value

Historically, private equity funds targeted a 3-to-5-year holding period before exiting through IPOs or strategic sales. In 2025, that model is shifting. Firms are increasingly holding investments for 7 to 10 years, focusing on operational improvements rather than financial engineering.

This trend reflects several factors:

- Debt is more expensive, reducing the attractiveness of high-leverage strategies.

- IPO markets remain unpredictable, delaying exits.

- LPs (limited partners) are emphasizing stable, compounding returns over short-term IRR spikes.

Some leading firms — such as Blackstone, KKR, and Carlyle — have launched “permanent capital vehicles”, which allow them to hold quality assets for longer periods and compound returns over time.

This approach not only aligns with LP expectations but also mitigates risk in volatile markets. The focus has shifted from quick wins to sustainable growth, where PE firms act more like long-term strategic partners than short-term financial sponsors.

Sector Focus: Resilience Over Hype

In 2025, private equity investors are gravitating toward sectors that offer defensive growth, predictable cash flows, and technological adaptability. While the tech boom of the early 2020s created immense value, the correction of 2023–2024 reminded investors that not all growth stories are sustainable.

Key focus areas include:

1. Technology with Real Utility

Rather than chasing speculative startups, PE firms are focusing on profitable, infrastructure-oriented tech companies — such as enterprise software, cybersecurity, and AI-driven business automation. These companies offer recurring revenue models and operational stability.

2. Healthcare and Life Sciences

Healthcare continues to attract strong investor interest. PE firms see long-term potential in areas such as biotech manufacturing, telehealth platforms, medical devices, and senior care, driven by aging populations and technological innovation.

3. Renewable Energy and Infrastructure

As sustainability becomes both an ethical and economic imperative, firms are increasing exposure to renewable energy projects, grid infrastructure, and green logistics. This shift aligns with ESG mandates from LPs and offers stable, inflation-protected cash flows.

4. Business Services and Essential Industries

In volatile markets, PE funds are turning toward mission-critical services — logistics, industrial automation, and software-as-a-service (SaaS) for supply chain management. These sectors provide steady margins and lower sensitivity to consumer demand cycles.

The underlying strategy is simple: invest where volatility creates opportunity, not vulnerability.

The Role of Debt Leverage in a New Rate Environment

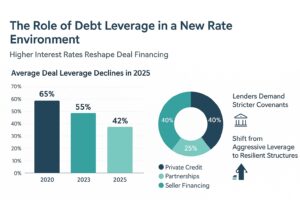

Leverage has long been the defining feature of private equity deals, but in 2025, that playbook is being rewritten. With central banks maintaining higher interest rates, debt-financed buyouts are becoming less attractive.

In previous cycles, firms could finance 60–70% of a deal with cheap debt. Now, average deal leverage sits closer to 40–45%, according to Bain & Company’s 2025 Global PE Outlook. Lenders have become more selective, demanding stricter covenants and preferring companies with consistent EBITDA growth and low cyclicality.

To adapt, firms are exploring alternative financing structures:

- Private credit partnerships: Collaborating with direct lenders and credit funds for flexible, tailored debt solutions.

- Seller financing: Negotiating deferred payments to reduce upfront capital outlay.

- Convertible debt: Balancing equity upside with fixed-income characteristics.

These adjustments reduce risk while maintaining deal momentum. The result is a more disciplined, data-driven approach to leverage, emphasizing resilience over aggressiveness.

Adapting Fund Strategies to a Shifting Macro Landscape

Private equity firms are not just reacting to volatility — they’re redesigning their operating models around it. Several trends define this evolution:

Operational Value Creation Takes Center Stage

Instead of relying on financial arbitrage, PE managers are focusing on operational transformation. This includes digital modernization, supply chain optimization, and workforce efficiency. Firms are hiring more operating partners with real industry expertise to drive value from within portfolio companies.

Data and AI in Portfolio Management

The integration of AI and analytics is changing how firms evaluate and manage investments. Predictive modeling, real-time performance dashboards, and AI-driven due diligence help PE teams identify risks and opportunities earlier, allowing faster decision-making in volatile conditions.

Co-Investment and Secondary Market Liquidity

To manage liquidity challenges, LPs are increasingly engaging in co-investments alongside general partners (GPs), reducing fees and improving transparency. Meanwhile, the secondary market for PE stakes continues to grow, providing investors with flexibility in otherwise illiquid assets.

ESG Integration

Environmental, Social, and Governance (ESG) factors are now integral to PE decision-making. Beyond compliance, firms recognize that ESG performance directly correlates with long-term value creation and downside protection.

The Rise of “Evergreen” and Long-Hold Funds

One of the most significant trends in 2025 is the rise of evergreen funds — vehicles that don’t have fixed lifespans. Unlike traditional funds that must return capital within 7–10 years, evergreen structures allow continuous reinvestment and compounding.

This flexibility enables firms to ride out market turbulence without being forced to sell during downturns. For LPs, evergreen models provide more consistent exposure to private markets without the need for constant re-commitment cycles.

Large institutions, family offices, and sovereign wealth funds increasingly favor this model for its predictability, lower volatility, and long-term alignment with asset management objectives.

Investor Sentiment and Future Outlook

Despite the challenges, investor confidence in private equity remains strong. The asset class continues to outperform public markets over long periods, and its active management model is particularly valuable in uncertain environments.

In 2025, investors are emphasizing risk-adjusted returns and portfolio diversification, seeking managers who can deliver consistent performance without overreliance on cheap debt or speculative valuations.

Private equity’s adaptability — its ability to evolve alongside macroeconomic conditions — remains its greatest strength. As one senior PE executive noted in a recent interview, “Volatility isn’t a threat; it’s a filter. It separates disciplined investors from lucky ones.”