Venture debt is a type of loan financing offered primarily to venture-backed startups that have already raised at least one round of equity funding. Unlike traditional bank loans that require profitability or hard assets as collateral, venture debt is based on a startup’s growth potential and investor backing.

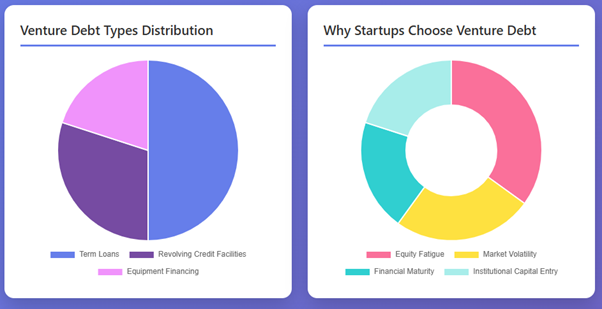

Lenders typically provide this capital as:

- Term loans – fixed-sum loans repaid over time, often used for expansion or product development.

- Revolving credit facilities – flexible funding lines that can be drawn upon as needed.

- Equipment financing – loans tied to the purchase of essential hardware or operational infrastructure.

In return, lenders often receive warrants — small equity rights that allow them to benefit if the startup performs well. This structure makes venture debt a hybrid instrument, blending the predictability of loans with the upside of equity.

The main attraction? Startups can raise capital without giving up ownership.

Why Venture Debt Is on the Rise

The venture debt market has expanded rapidly over the last five years, driven by macroeconomic shifts and investor caution. With interest rates rising globally and venture capital investors becoming more selective, many startups are finding equity rounds harder — and slower — to close.

According to PitchBook data, the U.S. venture debt market surpassed $30 billion in annual deployment by late 2024, while Europe saw an estimated 40% growth year-over-year. This surge highlights how debt is no longer a fallback plan; it’s now a strategic funding tool.

Key reasons for this growth include:

- Equity Fatigue: Founders are wary of excessive dilution after multiple VC rounds. Debt provides a way to scale while retaining control.

- Market Volatility: With unpredictable valuations, many startups prefer debt to delay equity raises until market conditions improve.

- Financial Maturity: As ecosystems evolve, both founders and lenders are more comfortable managing structured debt.

- Institutional Capital Entry: Private credit funds and institutional investors are entering the venture debt market, bringing sophistication and liquidity.

Venture debt, in essence, gives founders control, continuity, and capital efficiency — a rare combination in today’s competitive funding landscape.

The Strategic Benefits of Venture Debt

1. Non-Dilutive Growth Capital

Unlike equity financing, venture debt doesn’t dilute ownership. Founders maintain greater decision-making power, preserving the long-term value of their equity.

2. Extending the Runway

Many startups use venture debt to bridge funding rounds, giving them time to achieve milestones that justify higher valuations. For example, securing key clients or crossing revenue thresholds before the next equity raise.

3. Flexibility of Use

Funds raised via venture debt can support a wide range of needs — hiring, marketing, R&D, or geographic expansion — offering founders flexibility without external pressure from investors.

4. Strengthened Valuations

By achieving tangible growth with debt capital, startups can negotiate better terms and higher valuations in future funding rounds.

5. Lender Partnership Benefits

Reputable venture debt providers often become strategic partners, offering financial guidance, introductions, and even operational support — benefits that go beyond money.

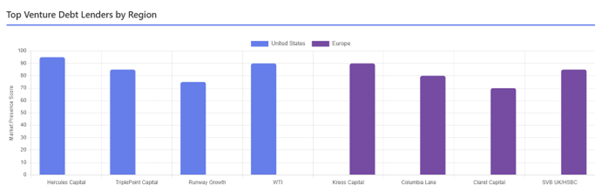

Key Venture Debt Players in the United States

The U.S. is home to the most mature venture debt ecosystem, powered by banks, business development companies (BDCs), and specialized private credit funds. Some of the key players include:

- Hercules Capital – A publicly listed BDC with deep experience in technology and life sciences lending. Known for providing flexible debt solutions to growth-stage companies.

- TriplePoint Capital – Focuses on high-growth tech and consumer companies, offering a mix of term loans and lines of credit.

- Runway Growth Capital – Specializes in customized lending structures designed around a startup’s growth cycle.

- Western Technology Investment (WTI) – One of the oldest venture debt firms, famous for supporting early-stage giants like Google, Facebook, and YouTube.

- Comerica Bank & Bridge Bank – Offer specialized innovation banking divisions catering to startups and venture-backed firms.

Even after the restructuring of Silicon Valley Bank (SVB), its influence continues to shape venture lending models across the ecosystem. Many lenders that emerged post-SVB have adopted similar frameworks with modern risk assessment tools.

The European Venture Debt Landscape

Europe has experienced a significant transformation in its venture financing ecosystem. Once heavily reliant on equity, European startups are now turning toward debt to complement their capital mix.

Prominent venture debt providers in Europe include:

- Kreos Capital – One of Europe’s largest and most established venture debt firms.

- Columbia Lake Partners – Known for flexible debt structures for SaaS and technology startups.

- Claret Capital Partners – Offers tailored loans to growth-stage companies across tech and life sciences.

- Silicon Valley Bank UK (under HSBC) – Continues SVB’s legacy of providing innovation-focused lending.

- European Investment Bank (EIB) – Plays a growing role in providing quasi-equity and debt instruments to innovative SMEs.

Regions like the UK, Germany, France, Sweden, and the Netherlands have seen rapid adoption of venture debt, especially in fintech, AI, and green tech sectors. The growth is supported by maturing ecosystems, investor confidence, and increasing availability of private credit.

Risks and Challenges: What Founders Must Know

Despite its advantages, venture debt is not suitable for every startup. It introduces repayment obligations that can strain cash flow if not planned properly.

Common challenges include:

- Repayment Pressure: Unlike equity, debt requires fixed repayment, which can burden early-stage startups with limited revenue.

- Restrictive Covenants: Some lenders impose performance-based conditions, restricting further fundraising or capital spending.

- Interest Costs: Rising interest rates globally have increased the cost of borrowing, making terms less favorable for some borrowers.

- Collateral and Warrants: While less demanding than traditional loans, venture debt still involves equity warrants and, in some cases, partial collateral.

Therefore, founders should carefully assess their cash flow, burn rate, and growth trajectory before signing a debt agreement.

Best Practices for Using Venture Debt Wisely

To make the most of venture debt, founders should approach it strategically. Here’s how:

- Time the Debt After an Equity Round

Lenders are more comfortable extending credit immediately after an equity raise, as investor confidence is high. This timing helps startups secure better terms and lower interest rates. - Use Debt for Strategic Growth

Debt should fund scalable activities such as expansion, product development, or acquisition — not operating losses. Using debt to stay afloat can create long-term financial strain. - Build Transparent Lender Relationships

Open communication with lenders fosters trust and flexibility. Regular updates on financials, milestones, and projections help establish a positive long-term relationship. - Understand the Fine Print

Founders must analyze terms related to warrants, prepayment penalties, and covenants before signing. The best deals are those that balance protection for the lender and flexibility for the borrower. - Align Debt with Growth Milestones

The borrowed capital should have a clear purpose — achieving measurable milestones like market entry, ARR targets, or a product launch — before the next equity round.

Case Studies: How Leading Startups Leveraged Venture Debt

- DoorDash (U.S.)

Before its IPO, DoorDash raised venture debt to expand logistics operations across North America. The capital injection helped it sustain rapid growth without heavy equity dilution before going public. - Revolut (UK)

The fintech leader strategically used venture debt to fund international expansion before its $800 million equity round. This allowed Revolut to negotiate from a position of strength and secure a higher valuation. - Northvolt (Sweden)

The clean energy startup raised billions through a mix of venture debt and project finance to fund its battery factory, proving that venture debt can fuel even capital-intensive industries. - Miro (Netherlands)

The SaaS collaboration platform utilized venture debt to expand its customer acquisition and enterprise sales teams globally before its Series C round.

These examples illustrate how venture debt is no longer just a bridge—it’s a growth accelerator.

The Future of Venture Debt: Tech, Data, and Global Expansion

The next phase of venture debt will be defined by technology and globalization.

- AI and Data-Driven Lending:

Lenders are increasingly using predictive analytics and AI-based risk models to assess startup potential beyond financial statements. This makes venture debt more accessible to early-stage, high-growth companies. - Rise of Private Credit Funds:

The global private credit market, now exceeding $2 trillion, is fueling venture debt expansion. Institutional investors are pouring funds into startup lending for higher returns than traditional fixed-income markets. - Emerging Markets Adoption:

Regions such as the Middle East, Southeast Asia, and Eastern Europe are witnessing a surge in venture debt adoption. As ecosystems mature, founders outside traditional hubs are discovering the power of non-dilutive growth capital.

Venture debt is evolving into a mainstream pillar of startup financing, complementing equity rather than replacing it.