Venture debt funding has surged to unprecedented levels in 2026, becoming the fastest-growing capital source for startups in the US, Europe, the Middle East, and North Africa (MENA). As global venture capital markets continue to recover from the funding contractions of 2023–2024, founders are increasingly turning to non-dilutive financing to extend runway, preserve ownership, and fuel expansion without waiting for equity valuations to fully rebound.

Analysts report that 2026 is on track to be the largest year ever recorded for venture debt, driven by aggressive activity from successor banks to Silicon Valley Bank (SVB), new fintech lenders, private credit funds, and regional development institutions across Europe and the Middle East. Startups across AI, cybersecurity, health tech, climate-tech, and B2B SaaS are leading demand, using venture debt to scale operations, enter new markets, and build product infrastructure.

US Venture Debt Market Hits New 2026 Peak Driven by Successor Banks and Private Credit

The US—traditionally the world’s largest venture debt market—has expanded sharply in 2026. The ecosystem that formed after SVB’s collapse has matured into a diverse, competitive lending environment dominated by players such as First Citizens Bank (SVB’s acquirer), Bridge Bank, Trinity Capital, Hercules Capital, Runway Growth Capital, and fintech-based lenders like Brex, Arc, and Pipe.

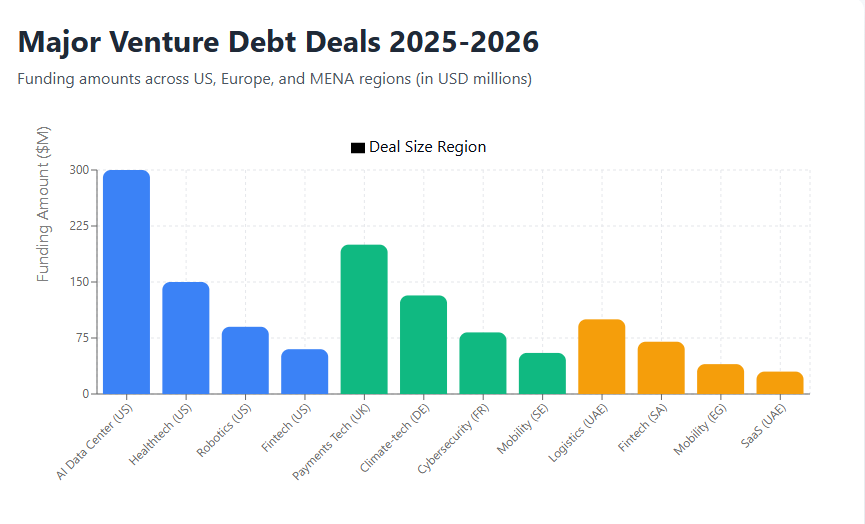

Major 2026 Venture Debt Deals in the US

The first two quarters of 2026 saw several landmark deals, including:

- $350 million debt facility for a leading AI semiconductor company scaling fabrication capacity in Arizona and Texas.

- $180 million venture debt package for a nationwide digital health platform integrating AI-driven diagnostics into hospital networks.

- $110 million financing deal for a robotics automation company serving major manufacturing and logistics enterprises.

- $85 million debt facility for a fintech API provider expanding credit infrastructure across North America and Europe.

These transactions signal a return of confidence from lenders who now consider venture-backed companies less risky than during the 2023–24 volatility period. Many lenders note that founders in 2026 are far more conservative with cash, using debt strategically to protect equity rather than as a last resort.

US venture debt issuance is projected to rise over 35% year-over-year, making 2026 one of the strongest years in the sector’s history.

Europe’s Venture Debt Uptake Accelerates Through 2026

Europe’s venture debt ecosystem has grown rapidly, now supported by a blend of innovation banks, private credit firms, and fintech lenders. Countries such as the UK, Germany, France, Sweden, Finland, and the Netherlands have reported significant growth in debt financing as startups prioritize capital efficiency.

HSBC Innovation Banking (the successor to SVB UK), Atempo Growth, Kreos Capital, Claret Capital, and multiple European Investment Bank–backed credit vehicles have expanded their loan book sizes in 2026.

Key European Venture Debt Deals of 2026

Among the most notable deals:

- £220 million facility raised by a UK-based payments infrastructure company expanding into the Middle East and Southeast Asia.

- €150 million funding line for a German battery-tech manufacturer scaling its green energy storage plants across Europe.

- €90 million debt round for a French AI cybersecurity firm serving enterprise and government clients.

- €60 million venture debt raise by a Dutch climate-tech startup building carbon capture installations.

The European market in 2026 is shaped by stricter equity fundraising conditions, pushing more startups to incorporate debt into their capital strategy. Growth-stage SaaS companies with predictable ARR and strong customer retention remain the most attractive targets for lenders.

Industry analysts expect Europe’s venture debt issuance to increase by 40% in 2026, marking its fastest growth period to date.

MENA Emerges as One of the Fastest-Growing Venture Debt Markets in 2026

The Middle East and North Africa region continues its rapid rise as a global technology and financing hub. Venture debt—previously a niche product—has become mainstream in 2026, backed by innovation funds, sovereign wealth initiatives, regional fintech lenders, and new private credit firms.

Saudi Arabia, the UAE, Egypt, and Bahrain are leading this wave, driven by national strategies focused on technology, logistics, fintech, and digital transformation.

Notable 2026 Venture Debt Deals Across MENA

Some of the biggest 2026 deals include:

- $120 million venture debt facility for a UAE-based logistics technology company expanding into Central Asia and East Africa.

- $85 million debt round for a Saudi fintech specializing in digital payments, payroll automation, and SME credit solutions.

- $50 million growth facility for an Egyptian mobility-tech startup launching cross-border fleet services.

- $35 million financing package for a Dubai-based SaaS company providing AI enterprise software for public sector modernization.

Lenders in the region highlight strong fundamentals: rising startup activity, robust government support, and a maturing investor ecosystem. Venture debt instruments are now considered essential tools for regional startups to achieve rapid growth while preserving founder equity.

The MENA venture debt market is projected to more than double in 2026, making it the region’s strongest year on record.

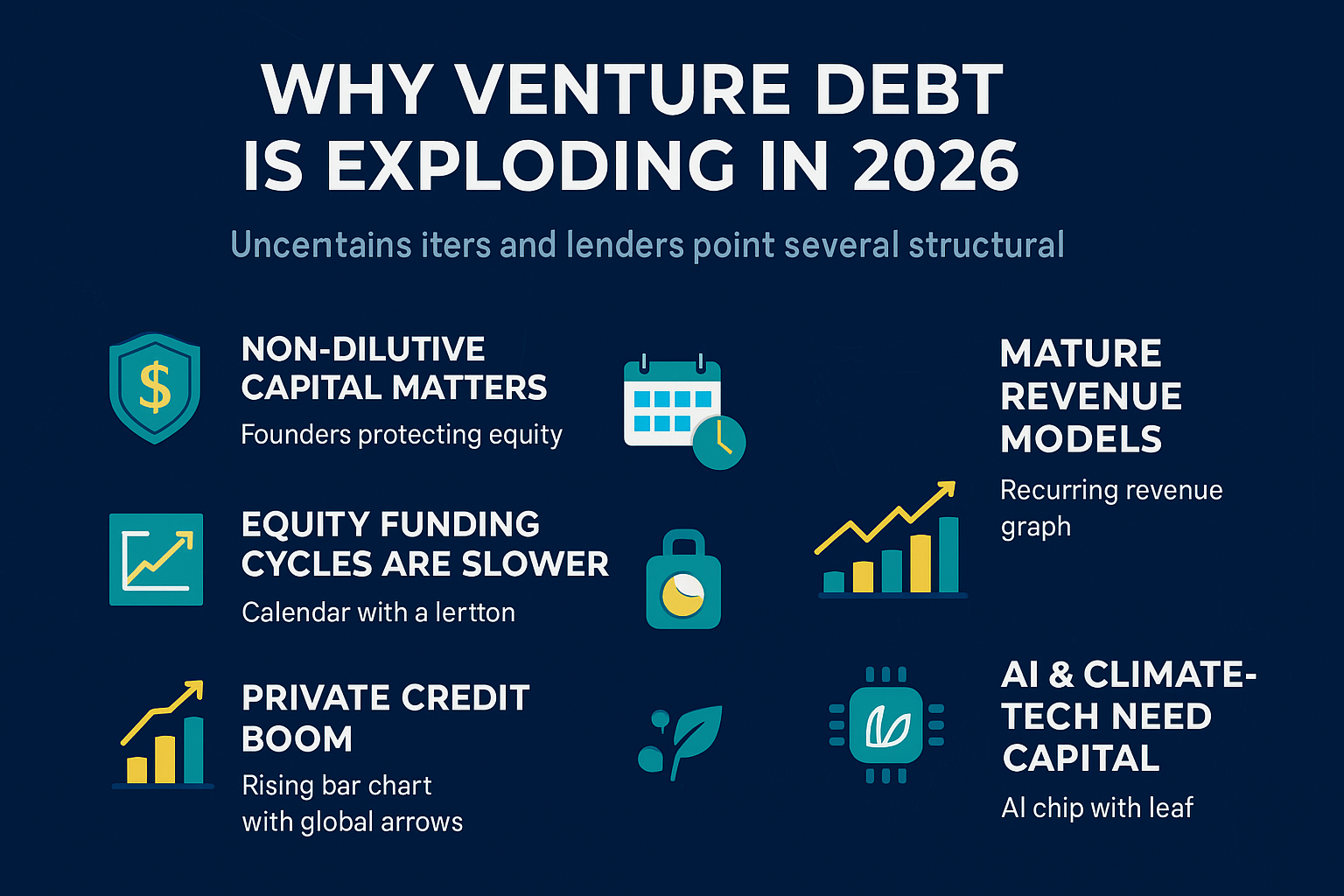

Why Venture Debt Is Exploding in 2026

Founders, investors, and lenders point to several structural reasons why venture debt has become the preferred financing tool in 2026.

1. Non-Dilutive Capital Is More Valuable Than Ever

After years of valuation fluctuation, founders want to protect equity and avoid down rounds. Venture debt allows startups to grow without sacrificing ownership.

2. Equity Funding Cycles Are Slower

Even though venture capital has recovered from the slowdown, equity rounds still take several months to close. Debt facilities often complete in weeks.

3. Revenue Models Have Matured

More startups in 2026 have predictable, recurring revenue—making them ideal candidates for debt underwriting.

4. Private Credit Is in a Global Boom

Private credit funds hold historic levels of dry powder, and venture debt offers attractive yields with manageable risk profiles.

5. AI and Climate-Tech Need Heavy Upfront Capital

These sectors require substantial infrastructure investment, and debt provides fast liquidity without giving up too much equity early on.

Lenders’ View: Why 2026 Is a Transformational Year for Venture Debt

Across the US, Europe, and MENA, lenders report several trends defining the 2026 landscape:

- The post-SVB era is fully stabilized, with multiple Banks replacing their market position.

- Risk assessment technologies are more advanced, using AI to model revenue, churn, burn rate, and unit economics.

- Fintech lenders have expanded eligibility criteria, delivering fast approvals based on ARR, revenue, and growth momentum.

- Competition has intensified, leading to more founder-friendly loan terms, including interest-only periods and flexible repayment structures.

Lenders say 2026 marks the first time venture debt is viewed not as supplemental capital, but as a strategic pillar of startup financing.

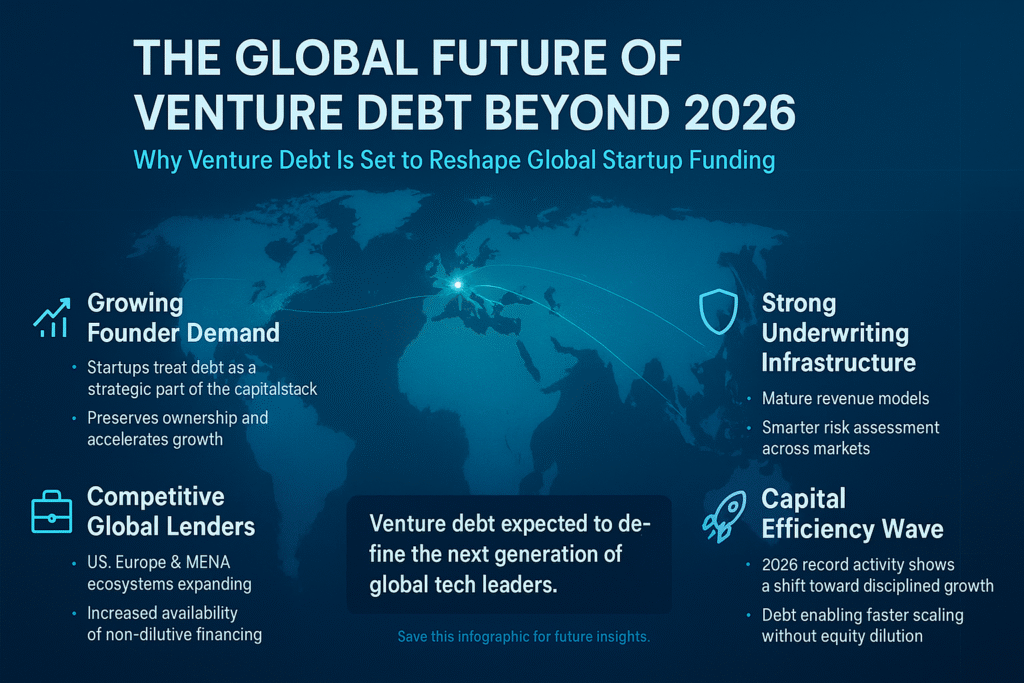

The Global Future of Venture Debt Beyond 2026

With strong underwriting infrastructure, rising founder demand, and competitive lenders across markets, venture debt is expected to continue expanding in 2027 and beyond. Startups now see debt as a deliberate component of their long-term capital stack rather than a fallback option. As financing ecosystems evolve across the US, Europe, and MENA, analysts predict that venture debt will play a defining role in building the next wave of global tech leaders.

The record-setting activity in 2026 reflects a broader shift toward capital efficiency, financially disciplined growth, and smarter structuring of investment strategies. In a world where founders want to scale fast without sacrificing control, venture debt has become one of the most powerful tools shaping the future of the global startup economy.