The U.S. venture capital (VC) market remains a global powerhouse despite economic uncertainty, policy scrutiny, and a cooling fundraising climate. According to the National Venture Capital Association’s (NVCA) 2025 Yearbook, U.S. VC firms closed an estimated $215.4 billion in deals during 2024, representing 57% of total global venture activity.

At the same time, NVCA data highlights an unprecedented level of “dry powder” — $307.8 billion in unspent capital waiting on the sidelines. This dual reality — record reserves amid slower deployment — defines the current investment landscape, positioning the U.S. as both the engine and the gatekeeper of the global startup economy.

Record Dry Powder Signals Strength Amid Caution

The NVCA report paints a fascinating picture of investor behavior heading into 2025. While fundraising slowed modestly from the 2021–2022 boom, venture firms are sitting on the largest cash reserves in history, reflecting both investor confidence in the asset class and uncertainty about when to deploy capital.

“Dry powder” refers to committed but uninvested capital in VC funds. The $307.8 billion figure marks a new all-time high, surpassing even the levels seen at the peak of the tech investment frenzy. Analysts say this capital build-up is not a sign of weakness but rather a strategic pause, as investors wait for valuations to normalize and exit opportunities to stabilize.

According to NVCA CEO Bobby Franklin, “The U.S. remains the world’s leading innovation economy, but firms are being more disciplined. There’s plenty of capital ready to be deployed — it’s just a matter of timing, pricing, and confidence in exit markets.”

This abundance of available cash gives U.S. venture funds an advantage as markets recalibrate. When valuations settle and IPO activity revives, these firms will be in a position to strike quickly — potentially fueling another strong investment cycle.

Fundraising Slowdown Reflects Market Realignment

Despite record reserves, fundraising momentum has cooled. In 2024, the number of new venture funds raised fell approximately 20% year-over-year, signaling a more selective environment for general partners (GPs) seeking commitments from limited partners (LPs).

Institutional investors — such as pension funds, endowments, and sovereign wealth funds — have become more cautious amid higher interest rates and macroeconomic uncertainty. Many LPs are rebalancing their portfolios after years of heavy exposure to private markets, preferring to hold back commitments until returns stabilize.

This has led to a bifurcation in the VC ecosystem:

- Top-tier firms like Andreessen Horowitz, Sequoia, and General Catalyst continue to raise billion-dollar-plus funds with relative ease.

- Emerging managers, however, face longer fundraising cycles and greater scrutiny.

Data from PitchBook and NVCA show that first-time funds represented less than 10% of total capital raised in 2024, one of the lowest shares in the past decade.

The result? A concentration of power among large, established firms with deep LP relationships — and a more competitive environment for smaller players trying to carve out their niche.

Deal Activity Shifts Toward Quality and Later Stages

While total capital deployed remained strong, deal volume declined, indicating a more selective approach from investors. The NVCA Yearbook reports that the number of U.S. venture deals fell by roughly 15% in 2024, even as total dollar value stayed robust.

This means investors are writing bigger checks but into fewer companies. The average deal size increased to $28 million, driven by late-stage and growth investments in sectors like artificial intelligence, cybersecurity, clean energy, and enterprise software.

Early-stage startups, by contrast, saw more modest funding, as investors demanded clearer paths to profitability and more disciplined capital usage. Seed and pre-seed founders found the environment especially challenging, with deal counts dropping nearly 25% year-over-year.

Yet, optimism remains. As valuations have adjusted downward since the highs of 2021, many VCs see 2025 as a buying opportunity — particularly in categories like AI infrastructure, climate tech, and digital health, where long-term growth prospects remain strong.

Policy Headwinds: Antitrust, Taxes, and Regulatory Uncertainty

The NVCA report also highlights how U.S. government policy is shaping the venture environment in new and complex ways. The Biden administration’s focus on antitrust enforcement, particularly against Big Tech and private equity roll-ups, has made some investors more cautious about consolidation-focused exit strategies.

Recent scrutiny from the Federal Trade Commission (FTC) and Department of Justice (DOJ) has slowed certain acquisitions, particularly in technology, health data, and fintech sectors. This increased oversight can delay exits — a key driver of venture returns — and may influence how investors structure deals in the coming year.

Tax policy is another looming concern. Discussions about potential increases to capital gains taxes and limits on carried interest deductions have added uncertainty to fund economics. While no major policy changes have been implemented yet, venture firms are actively lobbying for clarity and stability.

Despite these headwinds, NVCA emphasizes that regulation can also create opportunity — especially in climate innovation, infrastructure, and healthcare, where federal incentives and funding programs continue to attract capital.

Sector Trends: Where U.S. VC Is Investing in 2025

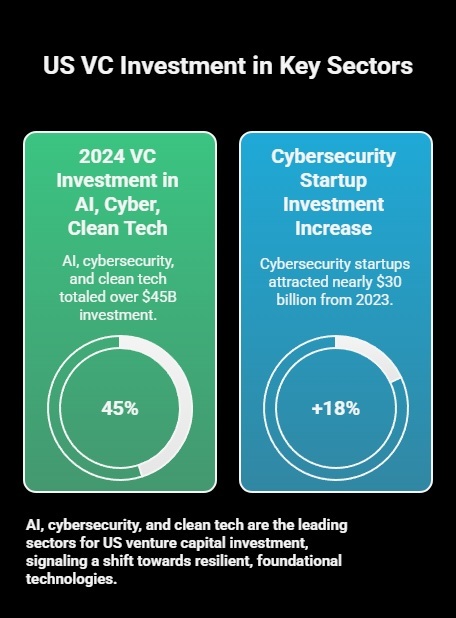

The composition of U.S. venture funding has evolved significantly since the pre-pandemic years. According to the NVCA Yearbook, 2024’s deal activity was dominated by AI, cybersecurity, and clean tech, which collectively accounted for over 45% of total VC investment.

Key Highlights:

- Artificial Intelligence (AI): Continued to lead with more than $65 billion invested across generative AI, data infrastructure, and applied enterprise tools.

- Cybersecurity: Spurred by high-profile breaches and global tensions, cybersecurity startups attracted nearly $30 billion, up 18% from 2023.

- Climate Tech: Investments surged as federal incentives under the Inflation Reduction Act accelerated innovation in energy storage, EV infrastructure, and carbon capture.

- Healthtech and Biotech: After a correction in 2023, digital health rebounded, driven by AI diagnostics and personalized medicine platforms.

This shift toward mission-critical and regulated sectors underscores a “flight to resilience” — a move away from consumer apps and toward foundational technologies that can weather macroeconomic turbulence.

The Global Context: U.S. Dominance Endures

Even amid fundraising challenges, the United States remains the undisputed leader in global venture capital. NVCA’s data shows that U.S. firms represented 57% of all global deal value in 2024, maintaining their dominant position over Asia and Europe combined.

This dominance reflects the deep maturity of the U.S. startup ecosystem — anchored by world-class research institutions, a large base of repeat founders, and a robust network of investors. Silicon Valley, New York, Austin, and Boston continue to attract the lion’s share of deals, though emerging hubs such as Atlanta, Denver, and Miami are quickly gaining traction.

Internationally, investors continue to view the U.S. as the most attractive market for innovation due to its scale, liquidity, and exit infrastructure — particularly through acquisitions and IPOs.

The Road Ahead: 2025 Outlook for Venture Capital

Looking ahead, the NVCA expects 2025 to be a transitional year for venture capital. With a record amount of dry powder available and valuations stabilizing, the market could see a resurgence of deal activity by mid-year.

Key factors shaping the outlook include:

- Interest rate stabilization, which could revive both M&A and IPO pipelines.

- AI and climate technology tailwinds are driving new waves of innovation and capital formation.

- Continued discipline among investors, with a focus on sustainable, long-term value creation.

However, risks remain. Prolonged regulatory uncertainty, geopolitical shocks, or another inflationary spike could delay a full recovery.

As NVCA’s Franklin summarized, “The capital is there, the innovation is there — what we’re waiting for is confidence.”

Conclusion

The NVCA Yearbook 2025 reveals a U.S. venture market that is both resilient and recalibrating. Despite fundraising slowdowns and policy headwinds, the combination of record dry powder, sectoral innovation, and a disciplined investor base positions the U.S. for another strong growth phase.

With over $215 billion deployed and $307 billion ready to invest, the message is clear: the U.S. remains the global heavyweight of venture capital — cautious in the short term but poised for a new era of intelligent, high-impact investment.