Global startup mergers and acquisitions (M&A) are witnessing a noticeable slowdown in 2026, as investors grow increasingly cautious amid ongoing market volatility, rising interest rates, and geopolitical uncertainties. Once considered a fast-track route to scale, liquidity, and innovation, startup M&A activity is now being reshaped by a more conservative investment climate.

Industry analysts point to a convergence of macroeconomic pressures and shifting investor sentiment as key drivers behind the slowdown. While dealmaking has not come to a complete halt, the pace, size, and risk appetite associated with acquisitions—particularly in the technology sector—have significantly declined compared to the post-pandemic surge seen between 2021 and early 2023.

Global Tech Acquisitions 2026: A Market in Transition

The global tech acquisition landscape in 2026 reflects a clear transition from aggressive expansion to strategic consolidation. Large corporations and venture-backed firms that previously pursued rapid acquisitions are now prioritizing profitability, operational efficiency, and long-term sustainability.

Data from multiple market trackers shows that total deal value in startup M&A has dropped by nearly 25–30% year-over-year. More notably, mega-deals—transactions exceeding $1 billion—have become increasingly rare. Instead, smaller, highly strategic acquisitions are dominating the landscape.

This shift is particularly evident in sectors like fintech, SaaS, and e-commerce, where valuations have corrected sharply. Buyers are no longer willing to pay premium multiples for growth alone; instead, they are focusing on fundamentals such as revenue stability, customer retention, and clear paths to profitability.

Investor Sentiment Turns Defensive

Investor behavior in 2026 has taken a defensive turn, influenced by persistent inflation concerns, tighter monetary policies, and global economic uncertainties. Interest rate hikes across major economies have increased the cost of capital, making leveraged buyouts and large acquisitions less attractive.

Venture capital firms, once known for their aggressive dealmaking strategies, are now exercising greater diligence. Many funds are reserving capital for existing portfolio companies rather than pursuing new acquisitions. This has directly impacted startup M&A trends, reducing both deal frequency and competitive bidding scenarios.

Private equity players, too, are recalibrating their strategies. While they remain active, their focus has shifted toward distressed assets and undervalued startups rather than high-growth, high-risk ventures.

Cross-Border M&A Slowdown Adds Complexity

Cross-border M&A activity has been particularly affected by geopolitical tensions and regulatory scrutiny. Governments across regions have tightened foreign investment rules, especially in sensitive sectors such as artificial intelligence, data infrastructure, and cybersecurity.

The cross-border M&A slowdown is also being driven by currency fluctuations and trade uncertainties, which complicate deal structures and valuation negotiations. For startups seeking international buyers, this has resulted in longer deal cycles and increased due diligence requirements.

In regions like Europe and Asia, where cross-border deals were previously a major growth driver, companies are now leaning toward domestic acquisitions or strategic partnerships instead of full-scale mergers.

Valuation Corrections Reshape Negotiations

One of the most significant factors influencing startup M&A trends in 2026 is the ongoing correction in startup valuations. After years of inflated valuations fueled by abundant liquidity, the market is undergoing a reset.

Startups that once commanded high multiples are now facing down rounds or reduced acquisition offers. This has created a disconnect between founders’ expectations and buyers’ willingness to pay, leading to stalled negotiations and fewer closed deals.

Acquirers are leveraging this environment to negotiate more favorable terms, including earn-outs, performance-based payouts, and deferred payments. While this reduces upfront risk for buyers, it adds uncertainty for founders and investors looking for immediate returns.

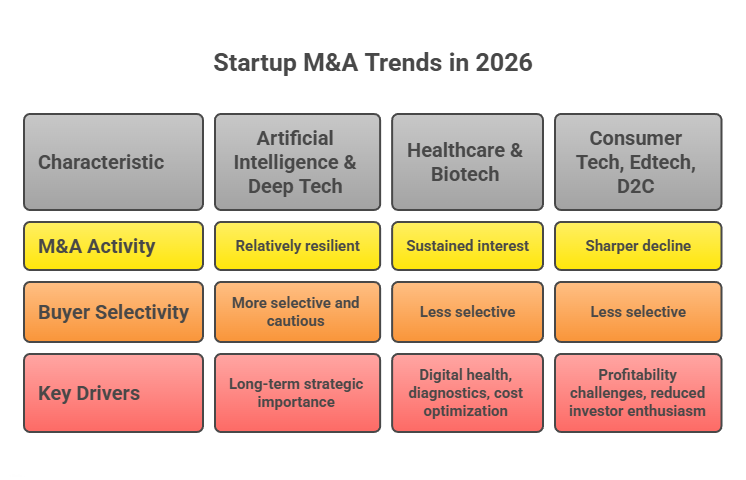

Sector-Wise Impact: Winners and Losers

The slowdown in startup M&A is not uniform across all sectors. Certain industries continue to attract acquisition interest, albeit at more measured levels.

Artificial Intelligence and Deep Tech remain relatively resilient, driven by long-term strategic importance and competitive pressures among major tech players. However, even in these sectors, buyers are more selective and cautious.

Healthcare and biotech startups are also seeing sustained interest, particularly in areas related to digital health, diagnostics, and cost optimization. The global focus on healthcare efficiency continues to support deal activity here.

On the other hand, sectors like consumer tech, edtech, and direct-to-consumer (D2C) brands are experiencing a sharper decline in M&A activity. Many of these startups are grappling with profitability challenges and reduced investor enthusiasm.

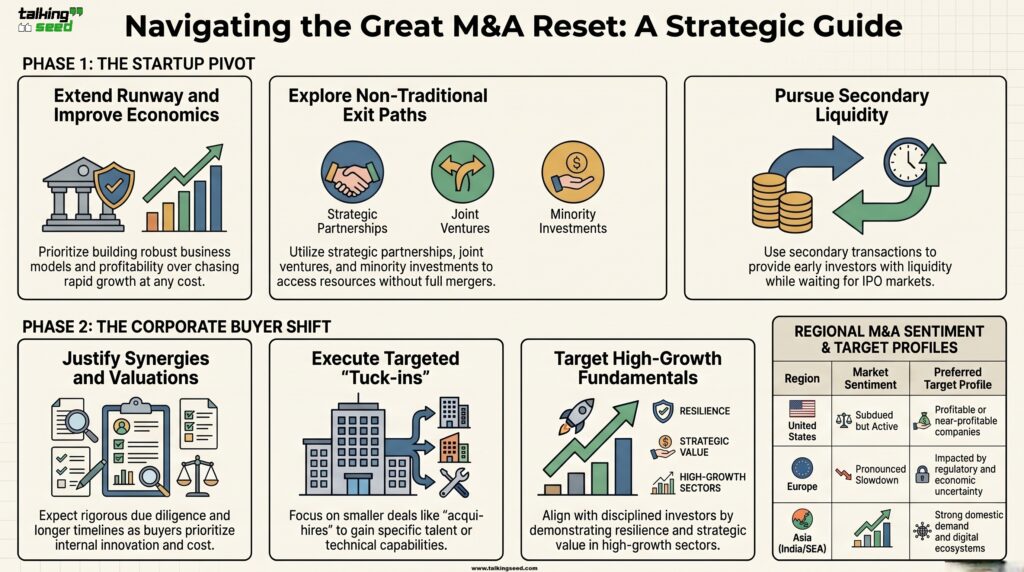

Startup Survival Strategies in a Slower M&A Market

With exit opportunities becoming less predictable, startups are being forced to adapt their strategies. Instead of relying on acquisitions as a primary exit route, many are focusing on extending their runway, improving unit economics, and exploring alternative funding options.

Strategic partnerships, joint ventures, and minority stake investments are emerging as viable alternatives to full acquisitions. These approaches allow startups to access resources and market opportunities without the complexities of a complete merger.

Some startups are also revisiting initial public offerings (IPOs), although market conditions remain challenging. Others are pursuing secondary transactions to provide liquidity to early investors.

Corporate Buyers Shift Focus

Large corporations, traditionally key drivers of startup M&A, are also adjusting their approach. Rather than pursuing aggressive expansion through acquisitions, many are prioritizing internal innovation and cost control.

Corporate development teams are now under greater pressure to justify deal valuations and demonstrate clear synergies. This has resulted in more rigorous due diligence processes and longer deal timelines.

In addition, companies are increasingly favoring “acqui-hires” and technology tuck-ins—smaller deals focused on acquiring talent or specific capabilities—over large-scale mergers.

Impact on Venture Capital Ecosystem

The slowdown in startup M&A deals has significant implications for the broader venture capital ecosystem. With fewer exits, funds are experiencing longer holding periods and delayed returns.

This, in turn, is affecting fundraising cycles, as limited partners become more cautious about committing new capital. The ripple effect is being felt across early-stage startups, which are facing tighter funding conditions and increased competition for investment.

However, some industry experts view this phase as a necessary correction that could lead to a healthier and more sustainable ecosystem in the long run.

Regional Trends: Diverging Patterns

While the overall trend points to a slowdown, regional dynamics vary significantly.

In the United States, the startup M&A market remains active but subdued, with a clear preference for profitable or near-profitable companies. Silicon Valley, long a hub for high-value acquisitions, is seeing a shift toward smaller, strategic deals.

Europe is experiencing a more pronounced slowdown, influenced by economic uncertainties and regulatory complexities. Cross-border deals within the region have also declined, reflecting broader geopolitical concerns.

In Asia, the picture is mixed. While China’s tech sector faces regulatory challenges, markets like India and Southeast Asia continue to show resilience, driven by strong domestic demand and growing digital ecosystems.

Outlook for Startup M&A Trends

Despite the current slowdown, experts believe that startup M&A activity will not remain subdued indefinitely. Market cycles are inherently dynamic, and periods of correction often pave the way for future growth.

As inflation stabilizes and interest rates eventually normalize, investor confidence is expected to improve. This could reignite dealmaking activity, particularly in high-growth sectors with strong fundamentals.

In the meantime, the current environment is likely to favor disciplined investors and well-managed startups that can demonstrate resilience, profitability, and strategic value.

A Reset Rather Than a Decline

The slowdown in startup M&A deals in 2026 should not be viewed solely as a negative development. Instead, it represents a broader reset in the global investment landscape.

The era of easy capital and aggressive valuations has given way to a more measured and sustainable approach. For startups, this means focusing on building robust business models rather than chasing rapid growth at any cost.

For investors and acquirers, it presents an opportunity to make more informed decisions and invest in companies with genuine long-term potential.

As the global market continues to navigate uncertainty, one thing is clear: the rules of the startup M&A game are changing, and adaptability will be the key to success in this new era.