November 2025

After nearly two years of contraction, global venture capital funding has staged a remarkable rebound in 2025, signaling renewed investor confidence in innovation and early-stage entrepreneurship. The resurgence is being driven by a sharp rise in funding for artificial intelligence (AI), climate technology, and fintech startups, according to recent data from global investment trackers.

Industry analysts note that early-stage deals — particularly seed and Series A rounds — are at the center of this recovery, reflecting a shift toward disciplined, fundamentals-based investing after the exuberant valuations of 2021 and 2022.

A Global Turnaround in Venture Confidence

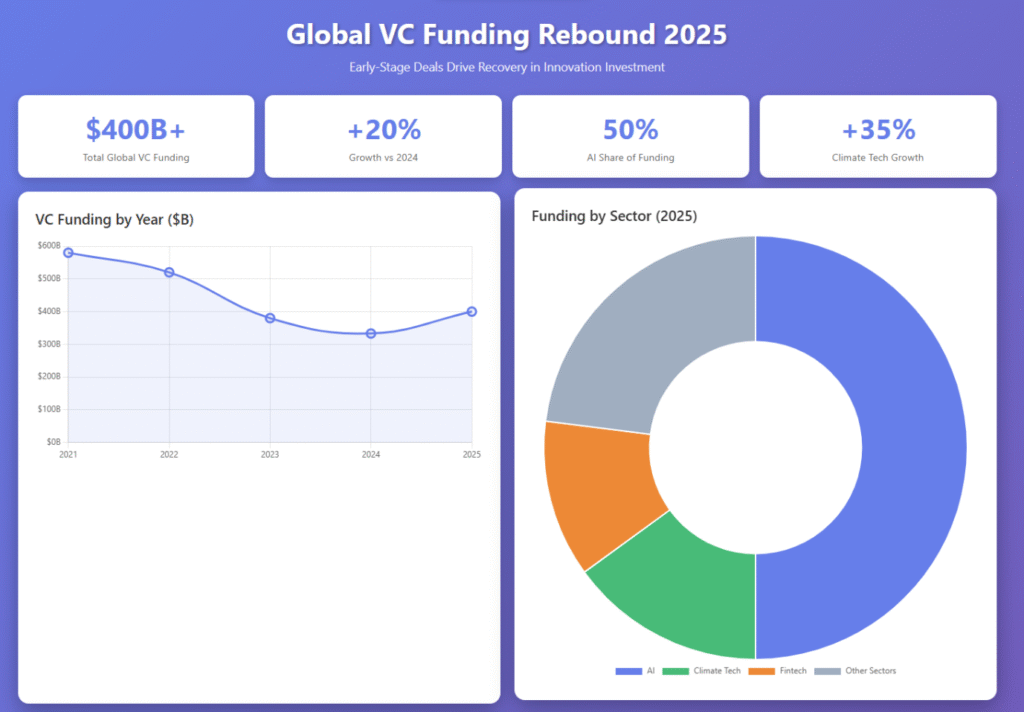

Global venture investment in 2025 has crossed the $400 billion mark, up more than 20 percent from 2024. Quarterly funding levels have remained consistently strong throughout the year, reversing the sluggish pace that characterized the previous downturn.

This upward trend suggests that venture capital is entering a new phase of stability. The appetite for funding innovative startups has returned, but with a sharper focus on quality, sustainability, and real-world impact.

Analysts highlight that while mega-rounds remain fewer than in the pandemic-era boom, the breadth of deal activity is widening again. The number of early-stage transactions is increasing, and investors are showing particular enthusiasm for startups building next-generation technologies that address productivity, climate resilience, and digital finance.

Early-Stage Deals Lead the Charge

Unlike the funding waves of the past, the 2025 rebound is being led from the ground up. Early-stage startups are attracting a larger share of total venture dollars, marking a fundamental change in market dynamics.

Seed and Series A rounds now account for more than half of global deal activity, up from roughly 40 percent two years ago. At the same time, the average deal size has grown by nearly 30 percent, as founders seek larger early rounds to extend runway and reduce dependency on uncertain follow-on capital.

Investors, meanwhile, are adopting a “fewer but better” approach — backing teams with proven technical depth, early traction, and a clear path to monetization. This signals a return to the venture model’s core principle: building value through innovation, not speculation.

A venture partner at a leading US firm summarized the trend succinctly: “The correction was painful, but it has cleaned up the market. The companies getting funded now are the ones that deserve to be.”

Artificial Intelligence Remains the Engine of Growth

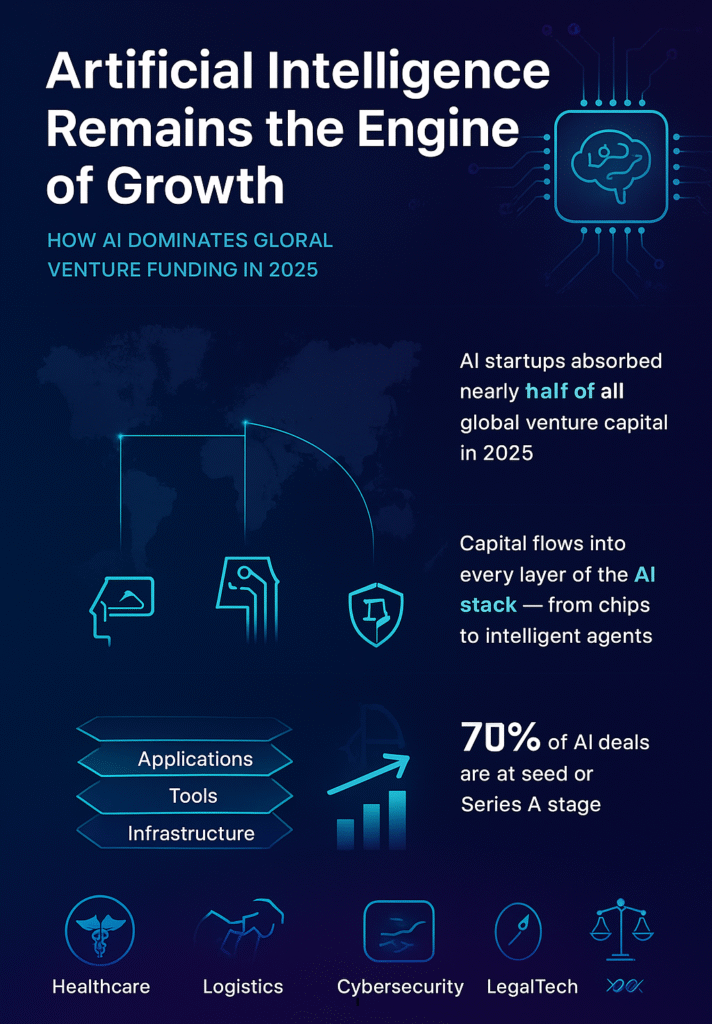

If one sector defines 2025’s recovery, it is artificial intelligence. AI startups have absorbed nearly half of all global venture funding this year, underscoring how deeply machine learning and automation have reshaped the investment landscape.

From model training and AI chips to intelligent agents and applied AI in healthcare, logistics, and cybersecurity, capital continues to flow into every layer of the AI stack. The biggest rounds of 2025 went to companies building AI infrastructure and tools that make generative and predictive systems more efficient, safer, and commercially scalable.

Crucially, the boom isn’t confined to late-stage giants. Over 70 percent of AI-related deals this year occurred at the seed or Series A level, showing that innovation remains vibrant at the grassroots. Smaller AI startups are being funded to explore niche and vertical-specific applications — from legal document automation to precision medicine — which investors believe will form the backbone of AI’s next wave.

Climate Tech Reclaims Investor Attention

Another bright spot in 2025’s investment landscape is climate technology. Global funding for the sector has surged 35 percent year-on-year as investors double down on energy transition and sustainability goals.

Unlike the speculative wave of a few years ago, today’s climate investments are more disciplined and data-driven. Startups are securing funding for technologies that deliver measurable impact — including battery storage, grid optimization software, green construction materials, and carbon management systems.

Government incentives, corporate net-zero mandates, and private-public partnerships are also driving the momentum. The result is a healthier ecosystem where both early innovation and industrial-scale deployment are being financed simultaneously.

An emerging trend is the rise of “climate SaaS” — software platforms that help industries monitor emissions, optimize energy use, and verify sustainability metrics. These scalable, capital-light solutions are particularly attractive to investors seeking faster returns within the climate sector.

Fintech Finds Its Footing Again

After a turbulent period of consolidation, fintech is back on investors’ radar. However, this time, it’s not about growth at all costs.

Venture investors have raised the bar for entry, demanding higher revenue, proven compliance, and profitability before investing. In 2025, the median annual recurring revenue (ARR) for fintech startups raising Series A rounds has risen to over $4 million — a sharp contrast to the early, high-burn models of the last decade.

Funding is now concentrated in segments such as embedded payments, B2B financial infrastructure, fraud prevention, and regulatory technology (RegTech). The recovery reflects not just investor interest, but also a global shift in how financial services is built and delivered — through APIs, automation, and embedded finance ecosystems.

As one European venture fund partner noted, “Fintech hasn’t slowed down — it’s matured. The winners now are those who blend technology with compliance and trust.”

Regional Dynamics: US Leads, Europe Strengthens, Asia Evolves

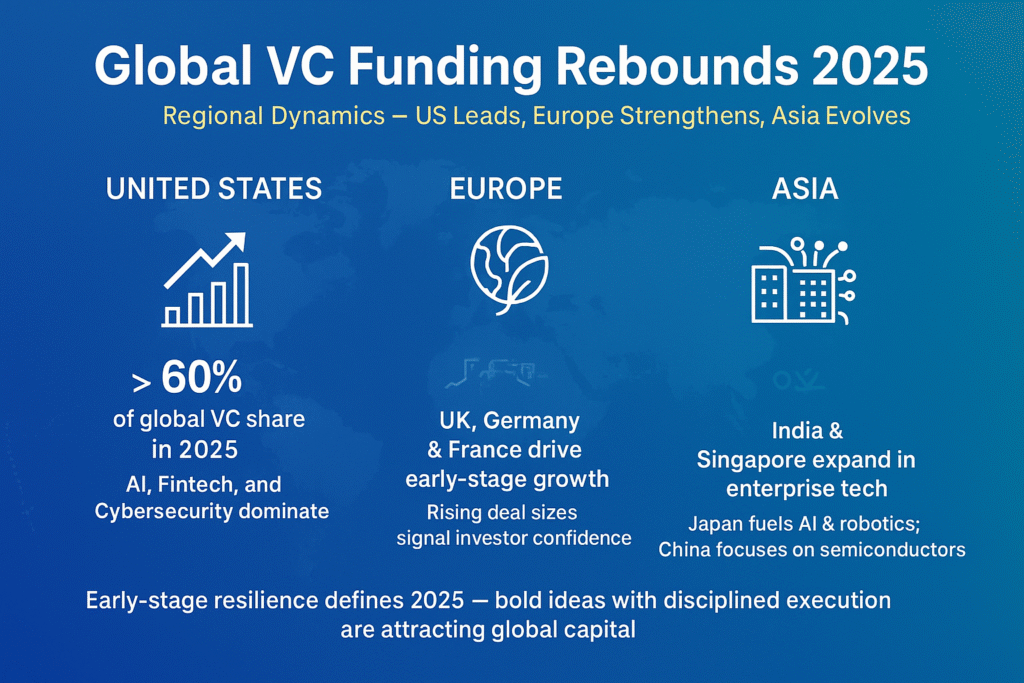

The United States continues to command the lion’s share of global venture capital activity, accounting for more than 60 percent of all investments in 2025. Silicon Valley remains the epicenter of AI innovation, while New York and Boston are strengthening their positions in fintech, biotech, and cybersecurity.

Europe is quietly emerging as a global leader in early-stage dealmaking. The UK, Germany, and France are home to a growing pool of climate and fintech startups attracting cross-border investment. European deal sizes have increased notably in 2025, signaling greater investor confidence in the scalability of regional ventures.

In Asia, the picture is mixed. India and Singapore continue to record healthy growth, particularly in enterprise tech and financial innovation, while Japan’s corporate-backed funds are fueling AI and robotics startups. China’s venture ecosystem, however, remains selective, with capital flowing primarily into strategic sectors such as semiconductors and energy technology.

Across regions, one trend stands out: early-stage resilience. Regardless of geography, investors are willing to bet on bold ideas — provided they are backed by solid execution and realistic financial models.

Exit Markets Begin to Reopen

For the first time since 2021, exit activity is showing signs of revival. Venture-backed IPOs and acquisitions have increased in both volume and value through 2025, providing long-awaited liquidity to investors.

While valuations remain moderate, the consistency of successful exits — particularly in AI and software sectors — is boosting confidence across private markets. Larger technology companies are once again acquiring startups to strengthen their AI and automation capabilities, creating healthy deal flow for venture funds.

This revival of the exit environment is crucial for maintaining the momentum of the current rebound. With more liquidity returning to the ecosystem, general partners are expected to accelerate new fund deployments heading into 2026.

From Speculation to Substance

The post-2021 correction forced the venture industry to rethink its approach. Gone are the days of reckless spending and unsustainable valuations. In their place is a more selective, substance-first mindset — one that prizes cash efficiency, clear business models, and long-term viability.

The companies emerging from this phase are stronger, leaner, and more strategically aligned with market realities. Investors describe the new environment as “healthier,” emphasizing patient capital and operational discipline over hypergrowth.

As a result, 2025’s venture ecosystem feels both smaller and more focused — but also far more sustainable. For the first time in years, innovation and capital seem to be moving in lockstep again.

A Foundation for the Next Cycle

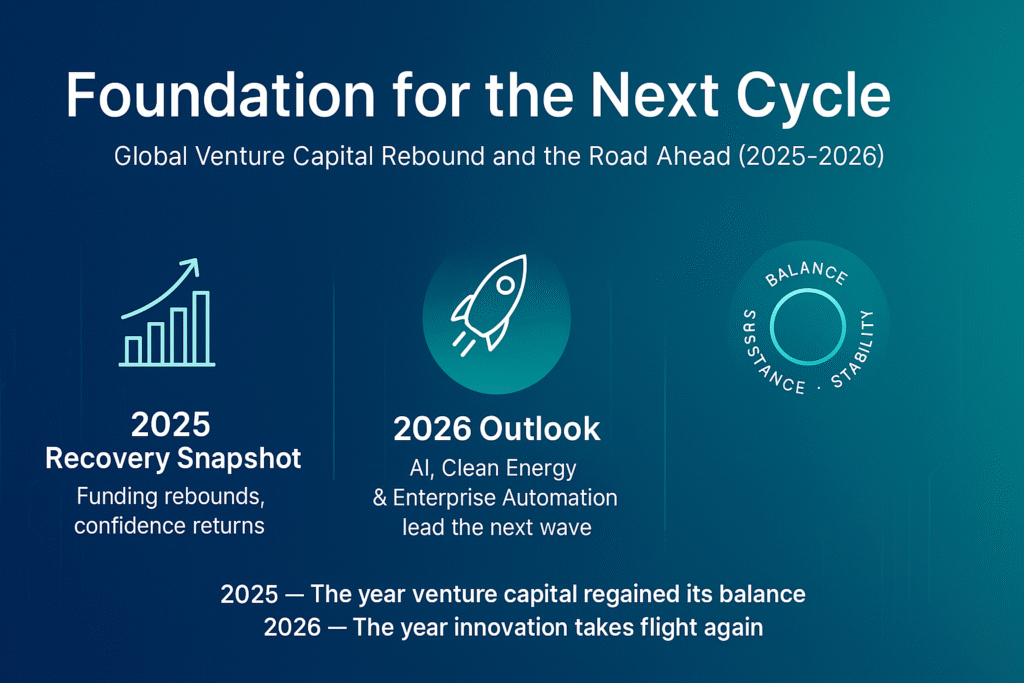

The rebound in global VC funding in 2025 is not merely a short-term recovery — it may mark the beginning of a new, more resilient era in venture capital. Early signs suggest that 2026 will continue this trajectory, with sustained growth across AI, clean energy, and enterprise automation.

While macroeconomic uncertainty remains, the fundamentals are improving: exits are reopening, investor confidence is rising, and the next wave of high-impact startups is already in motion.

If 2024 was the year of caution, 2025 became the year of recalibration. Now, 2026 is shaping up to be the year when venture capital reclaims its role as the engine of global innovation — powered not by speculation, but by substance, sustainability, and smart risk-taking.

In summary, 2025 will be remembered as the year the venture capital world regained its balance. With early-stage founders driving innovation and investors demanding stronger business fundamentals, the industry has entered a healthier, more disciplined phase — one that could define the next decade of global entrepreneurship.