Private equity firms are increasing their exposure to artificial intelligence (AI) infrastructure, specialized data centers, and automation-focused startups as the technology sector adjusts to an extended market correction. Dealmakers say investment activity has shifted toward companies that supply critical computing capacity, operational automation, and secure data-handling environments, all of which are becoming essential for enterprises expanding their AI capabilities.

Analysts tracking PE activity report rising interest in high-performance computing providers, GPU-based cloud platforms, edge data center operators, and firms offering workflow automation and AI-enabled cybersecurity. Investors argue that these businesses offer stronger resilience, recurring revenue streams, and long-term service commitments, at a time when several traditional software and consumer-tech segments are experiencing slower growth and valuation pressure.

Infrastructure Assets Move to the Forefront

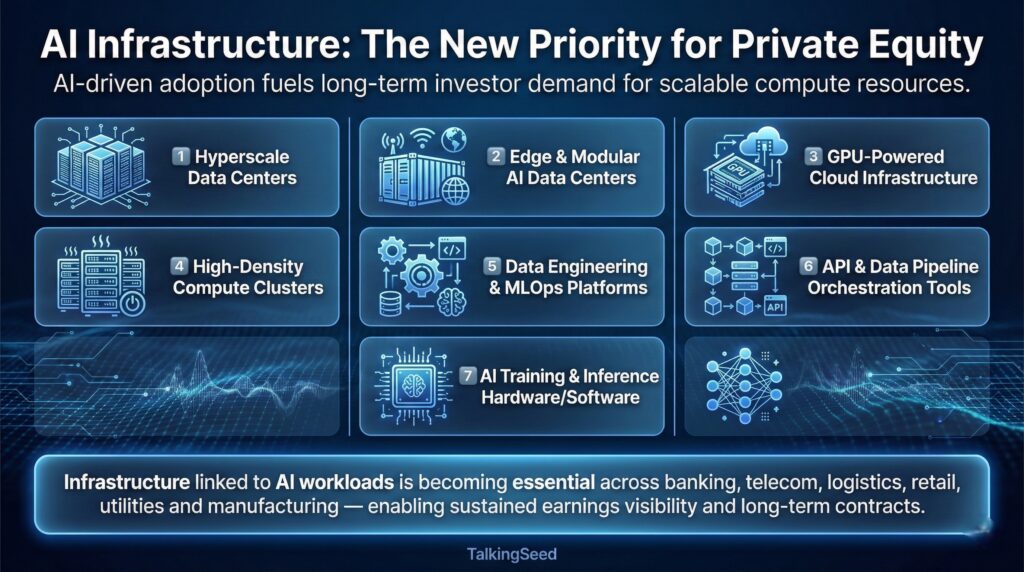

Private equity firms are prioritizing deals in infrastructure categories that support AI deployment at scale. The surge in enterprise adoption of generative AI, predictive analytics, and automated decision systems has created sustained demand for compute power, storage capacity, and orchestration tools.

Key segments attracting PE attention include:

- Hyperscale data centers

- Modular and edge data centers designed for low-latency AI workloads

- GPU-powered cloud infrastructure

- High-density compute clusters

- Data engineering and MLOps platforms

- API orchestration and data pipeline management tools

- Hardware and software supporting AI inference and training

Fund managers say that infrastructure tied to AI workloads is becoming non-negotiable for enterprises in banking, insurance, telecom, logistics, utilities, retail and manufacturing. Demand for scalable compute resources has grown rapidly as companies integrate generative AI into customer service, risk modeling, operations planning, marketing, fraud detection, and supply chain optimization.

Because infrastructure assets operate on long-term service contracts and subscription models, investors see greater earnings visibility compared to sectors dependent on discretionary consumer or advertising spending.

Automation Startups Gain Transaction Momentum

Automation remains a major focus for private equity due to strong demand from enterprises seeking cost reductions and operational efficiencies. Analysts say the current environment has accelerated automation adoption across industries that are dealing with rising operational expenses, evolving workforce structures, and pressure to deliver faster digital services.

PE firms are evaluating targets in:

- Enterprise workflow automation

- Predictive analytics used to optimize operations

- Finance and accounting automation

- AI-powered customer interaction systems

- Document processing automation

- Supply chain and logistics automation solutions

- Industrial IoT and robotics

Executives involved in deal sourcing report that automation companies are demonstrating consistent annual revenue growth driven by multi-year enterprise contracts. Many platforms have become embedded in core business processes, making them difficult for customers to replace. This factor improves revenue retention, a key metric for private equity deal models.

Data Centers Lead New Deal Pipelines

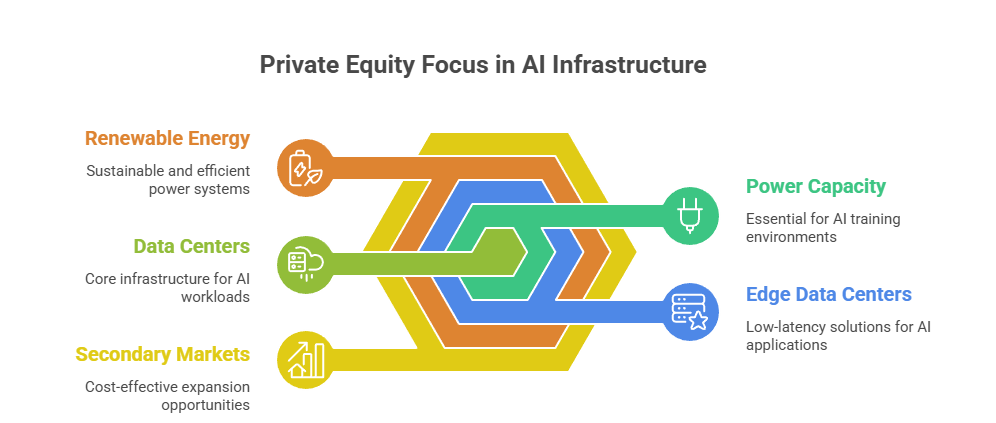

Among all AI-linked infrastructure categories, data centers remain the most active area for private equity funds. The rapid expansion of AI training and inference workloads is driving significant demand for high-density facilities capable of supporting GPU clusters and advanced cooling systems.

Investment committees are increasingly focusing on:

- Facilities with the power capacity to support large AI training environments

- Operators developing edge data centers for low-latency AI applications

- Facilities incorporating renewable energy or high-efficiency power systems

- Companies expanding into secondary markets with high demand and lower construction costs

- Operators offering managed hosting services for enterprise AI models

Industry specialists say growth in AI-related data consumption is outpacing traditional cloud workloads. Several operators are planning new builds or expansion phases to keep up with enterprise demand. These conditions have created a favorable environment for PE firms looking for consolidation opportunities or platform investments.

Data center revenues are typically based on long-term colocation or hosting contracts, which provide multi-year cash flow stability — a priority for private equity portfolios during uncertain economic periods.

Cybersecurity Infrastructure Gains Strategic Importance

The expansion of AI across business functions is increasing the volume of sensitive data flowing through enterprise systems. As a result, cybersecurity infrastructure has become a high-priority target for private equity investors seeking exposure to essential services with strong growth prospects.

Key investment areas include:

- Identity and access management platforms

- Cloud-native security systems

- Threat detection tools leveraging machine learning

- Data protection and encryption solutions

- Compliance automation technologies

- Infrastructure security for distributed AI systems

Cybersecurity providers benefit from enterprise demand that is less cyclical than discretionary technology spending. Deal teams report heightened interest in companies offering platforms that integrate security across hybrid cloud environments, especially those supporting AI-related workloads that require tighter governance.

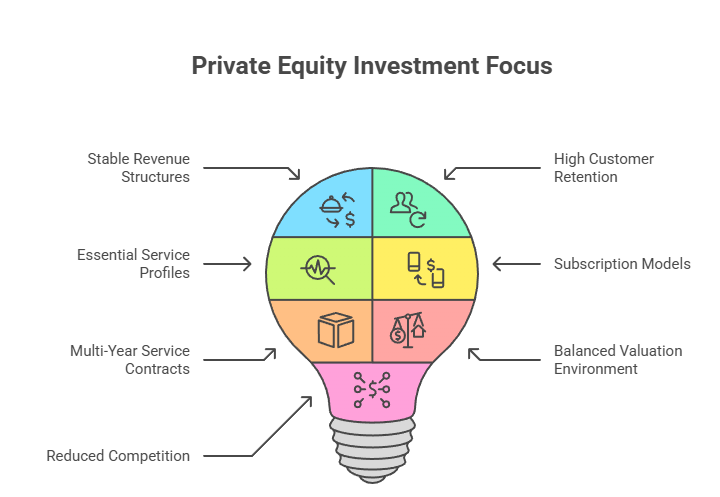

Shift Toward Predictable Revenue and Resilient Business Models

Private equity investors are placing greater emphasis on businesses with stable revenue structures, high customer retention, and essential service profiles. Infrastructure and automation companies generally operate on subscription models or multi-year service contracts, which provide cash flow predictability and reduce exposure to short-term market fluctuations.

Deal professionals say the correction in valuation expectations across the technology sector has also created a more balanced environment for acquisitions. Companies focused on AI infrastructure and automation remain relatively insulated due to rising enterprise demand, positioning them as preferred targets as funds seek long-term stability.

Industry analysts note that the combination of steady demand, reduced competition from overvalued tech sectors, and the recurring nature of infrastructure revenue is shaping investment priorities across major private equity firms.

Consolidation Expected Across AI Infrastructure Segments

Market observers expect continued consolidation as infrastructure providers compete to scale their capacity and meet rising enterprise requirements. Data center operators, GPU cloud providers, and automation platforms are increasingly exploring mergers, partnerships, and strategic acquisitions to expand coverage, secure power availability, and support larger client workloads.

Private equity firms are expected to play a significant role in this consolidation by providing capital for capacity expansion, operational upgrades, and acquisitions of smaller niche players. Analysts say the sector’s fragmentation makes it particularly attractive for buy-and-build strategies.

In the automation segment, consolidation is being driven by enterprise expectations for integrated platforms capable of handling multiple workflows. Investors are evaluating opportunities to combine complementary technologies across document automation, analytics, and workflow orchestration to create broader service offerings.

Deal Sourcing Accelerates as Valuations Stabilize

Investment banks and advisory firms report higher deal pipelines involving infrastructure and automation assets. As valuations stabilize at levels more aligned with growth fundamentals, private equity funds are finding improved entry points for strategic acquisitions.

Funds are prioritizing:

- Companies with high enterprise adoption

- Infrastructure tied directly to AI workloads

- Platforms showing strong retention and low churn

- Businesses that are cash-flow positive or near break-even

- Operators with expansion capacity or access to energy and land resources

Analysts expect deal activity to remain strong as PE firms deploy available capital into sectors positioned for long-term structural growth.